Landlord insurance sewer coverage is defined as a set of policy endorsements that protect rental property owners from financial losses caused by sewer backups and underground pipe failures, neither of which standard policies cover. Most landlords carry rental property insurance and assume they are fully protected. They are not. A single sewage backup can trigger Category 3 water contamination, requiring specialized remediation that costs far more than a year's worth of endorsement premiums. Two separate add-ons, water backup coverage and service line coverage, close this gap. Understanding both is the first step toward protecting your investment.

What does landlord insurance sewer coverage actually include?

Standard landlord policies treat sewer failures as maintenance issues, not insurable events. That means the cost of cleanup, pipe repair, and tenant displacement lands entirely on you unless you purchase specific endorsements.

Two endorsements provide comprehensive protection:

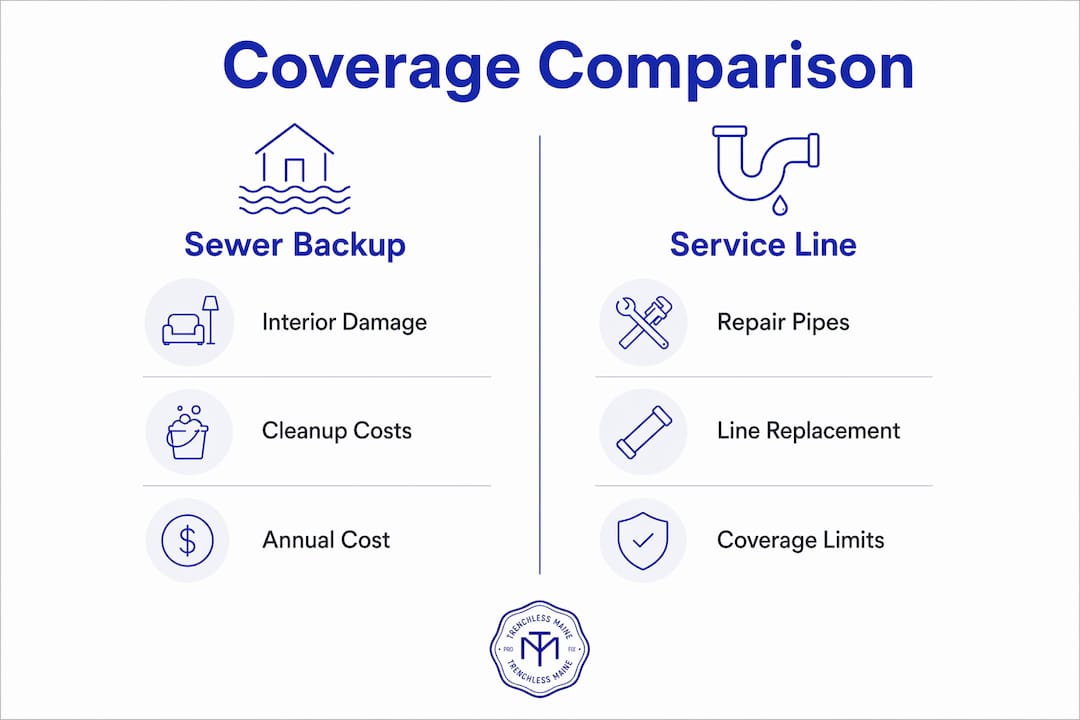

- Sewer backup coverage pays for interior damage caused by sewage flowing back into the property. This includes flooring, walls, personal property in common areas, and the cost of professional remediation.

- Service line coverage pays to repair or replace the underground pipes connecting your property to the municipal main. This covers the sewer lateral, water lines, and electrical conduits buried on your land.

These two products are distinct but complementary. Sewer backup coverage handles the mess inside the building. Service line coverage handles the broken pipe underground. You need both for full protection.

What service line coverage includes and excludes

Service line coverage pays for damage caused by root intrusion, freezing, and mechanical accidents. It does not cover wear and tear or corrosion. That distinction matters because older pipes in Maine often fail from corrosion, which insurers classify as a maintenance problem.

Common covered perils under service line coverage:

- Root intrusion cracking or collapsing a lateral line

- Ground freezing that fractures a water or sewer pipe

- Accidental mechanical damage from excavation nearby

- Sudden pipe deformation from soil movement

Common exclusions across both endorsements:

- Pre-existing pipe deterioration or corrosion

- Damage caused by neglected maintenance

- Flooding from surface water (covered under separate flood insurance)

- Pipe failures outside your property boundary (the municipality's responsibility)

Pro Tip: Repair costs for sewer line damage from root intrusion average $8,731, and water line ruptures can exceed $6,529. Set your coverage limits above those thresholds, not at them.

Coverage costs and typical limits

Sewer backup endorsements cost $50–$150 per year and coverage limits typically start at $5,000. Service line endorsements run slightly higher, with annual premiums ranging from $50 to $250 depending on property age and location. Given that landlord insurance premiums already run roughly 25% higher than standard homeowners insurance, adding both endorsements still costs a fraction of one claim payout.

| Coverage Type | What It Pays For | Typical Annual Cost | Typical Limit |

|---|---|---|---|

| Sewer backup | Interior cleanup and repairs | $50–$150 | $5,000–$25,000 |

| Service line | Underground pipe repair or replacement | $50–$250 | $10,000–full replacement |

How to evaluate your rental property's sewer risk

Not every rental property carries the same exposure. Your risk level depends on several concrete factors, and matching your coverage limits to your actual worst-case scenario is what separates a useful policy from a false sense of security.

Key risk factors to assess:

- Property age. Homes built before 1980 often have clay or cast iron lateral lines that crack, corrode, and attract root intrusion.

- Tree proximity. Large trees near sewer laterals are the leading cause of root intrusion failures.

- Basement presence. Basement units sit below the municipal main, making them far more vulnerable to backflow.

- Local infrastructure. Older municipal systems in many Maine cities combine storm and sanitary sewers, which overflow during heavy rain events.

- Sump pump condition. Properties with sump pumps require battery backup systems. Insurers often require battery backup as a condition of approving a sewer backup endorsement.

Municipal sewer authorities cover only the main line on their side of the property boundary. Everything from the main to your building, the sewer lateral, is your financial responsibility. Lawsuits against municipalities are slow and rarely successful. Insurance is the practical solution.

Understanding tenant and landlord responsibilities for water damage also shapes how you set coverage limits. If a backup damages a tenant's belongings, their renters insurance covers their personal property. Your policy covers the building and common areas. Knowing that boundary prevents you from over-insuring or under-insuring either side.

Pro Tip: Schedule a camera inspection of your sewer lines before applying for coverage. The inspection report documents current pipe condition and strengthens your position if you ever need to file a claim.

How to add sewer backup coverage to your landlord policy

Adding these endorsements is straightforward, but preparation makes the process faster and improves your chances of getting favorable terms.

- Contact your current insurer first. Ask specifically about water backup and service line endorsements. Not every carrier offers both, and some bundle them.

- Answer the property questions accurately. Insurers will ask about pipe material, property age, basement presence, and whether you have a sump pump with battery backup.

- Gather your documentation. Prepare recent inspection reports, maintenance receipts, and any records of prior plumbing repairs. This documentation proves the property is in good condition.

- Request coverage limits above your worst-case cost. Use the $8,731 average for root intrusion repairs and the $6,529 figure for water line ruptures as your floor, not your ceiling.

- Review the declarations page after the endorsement is added. Confirm the coverage limits, deductibles, and covered perils match what you discussed with your agent.

- Set a calendar reminder to review annually. Pipe infrastructure ages, and your coverage limits should keep pace with rising remediation costs.

Deductibles for sewer backup endorsements typically run $500–$1,000. Choosing a higher deductible lowers your premium but increases your out-of-pocket cost per claim. For landlords with multiple properties, a lower deductible often makes more sense because the risk of a claim is higher across a larger portfolio.

Common challenges when filing a sewer backup claim

Filing a claim is where many landlords lose money they thought they had covered. Insurers require proof that the damage was sudden and accidental, not the result of deferred maintenance.

Claim documentation requirements include:

- Pipe age and material records

- Recent inspection reports showing the pipe was in acceptable condition

- Maintenance receipts for any prior repairs or cleaning

- Photos and video of the damage taken immediately after the event

- A written remediation estimate from a licensed contractor

Claims get denied for predictable reasons. A pipe that shows years of root intrusion without any maintenance history reads as a neglected maintenance issue, not an accidental event. A basement that flooded repeatedly before the endorsement was added may be flagged as a pre-existing condition.

Pro Tip: Sewage backup is Category 3 water contamination, which requires specialized remediation companies, not general contractors. Hiring the wrong crew can void your claim or leave hidden mold that creates future liability.

Proactive communication with your insurer also matters. Notify them immediately after a backup occurs. Do not begin cleanup or repairs before an adjuster documents the damage. Premature cleanup is one of the most common reasons insurers reduce or deny payouts.

Selecting appropriate coverage limits is equally critical. Low limits leave you paying out of pocket for professional sewage remediation, which involves hazardous waste handling and can run well above basic repair estimates. Match your limits to the realistic cost of a full remediation in your area, not the minimum the insurer offers.

Key Takeaways

Landlords who carry both sewer backup and service line endorsements are the only ones fully protected against the two most common and costly underground failures that standard rental property insurance excludes.

| Point | Details |

|---|---|

| Standard policies exclude sewer damage | You must add water backup and service line endorsements separately to close this gap. |

| Two endorsements are required | Sewer backup covers interior cleanup; service line coverage pays for underground pipe repair. |

| Root intrusion repairs average $8,731 | Set coverage limits above this threshold to avoid out-of-pocket exposure on a single claim. |

| Documentation prevents claim denials | Keep inspection reports, maintenance receipts, and pipe records current before any damage occurs. |

| Annual review is non-negotiable | Pipe infrastructure ages and remediation costs rise, so coverage limits need regular adjustment. |

Why I think most landlords are one backup away from a serious loss

I have reviewed enough landlord claims to see a clear pattern. The landlords who get hurt are not the ones who skipped insurance entirely. They are the ones who assumed their standard rental property insurance covered everything underground. It does not, and that assumption is expensive.

The misconception is understandable. Homeowners insurance with sewer coverage is sometimes marketed as a complete package, and landlords carry that mental model into their rental property policies. But landlord liability insurance operates under different rules, and the exclusions are broader.

What I find most frustrating is how affordable the fix is. Spending $150–$400 per year on both endorsements is genuinely one of the best risk-adjusted decisions a landlord can make. The math is not close. One sewage backup in a basement unit, with Category 3 remediation, tenant relocation costs, and pipe repair, can easily reach $20,000 or more.

My advice: pull out your current declarations page today. If you do not see water backup and service line coverage listed as endorsements, call your agent this week. And schedule a professional sewer inspection before you apply. It documents your pipe condition, which protects you at claim time and may lower your premium.

— John

Trenchlessmaine helps landlords stay ahead of sewer problems

Preventing a sewer backup is always less expensive than filing a claim. Trenchlessmaine specializes in the exact services Maine landlords need to keep their sewer lines clean, documented, and defensible to insurers.

Trenchlessmaine's hydro jetting service uses high-pressure water to clear root intrusion, grease buildup, and debris from sewer laterals before they cause a backup. The service also produces documentation you can attach to an insurance application or claim file. For landlords who need faster results, drain clearing in Maine resolves active blockages quickly, often within 24 hours. Trenchlessmaine serves most of Maine's cities and backs its work with industry-leading warranties. Contact Trenchlessmaine to schedule an inspection or maintenance visit before your next lease renewal.

FAQ

Does standard landlord insurance cover sewer backups?

Standard landlord insurance does not cover sewer backups. You must add a water backup endorsement and a service line endorsement separately to gain that protection.

How much does sewer backup coverage cost for a rental property?

Sewer backup endorsements typically cost $50–$150 per year. Service line coverage runs $50–$250 annually, making both endorsements affordable relative to the cost of a single claim.

What is the difference between sewer backup and service line coverage?

Sewer backup coverage pays for interior damage and cleanup caused by sewage backflow. Service line coverage pays to repair or replace the underground pipe itself. You need both for complete protection.

Can a sewer backup claim be denied?

Yes. Insurers deny claims when damage appears to result from deferred maintenance rather than a sudden accidental event. Keeping inspection reports and maintenance receipts current is the best defense against denial.

Who is responsible for the sewer lateral connecting my rental to the city main?

The landlord is responsible for the sewer lateral from the property boundary to the building. Municipal authorities cover only the main line on their side, leaving lateral repair costs entirely with the property owner.